Countries across Asia Pacific have become global leaders at delivering instant payments through digital banking solutions. Their experimentation and innovation around alternative payment rails to better facilitate both cross-border and domestic instant payments serves to bolster the region’s growing stature and leadership across the payments sector.

In recent years, APAC has grown to dominate the digital banking sector, with 20% of approximately 250 digital banks worldwide based in the APAC region.

Regional leaders to highlight include: Singapore — ranked in the world’s top five most competitive financial centers — which has enacted clear and effective governmental regulation and support of innovative payment technologies and achieved a 58% increase in instant payments in 2021. And the Philippines, which saw virtual currency transactions jump 71% from 2020 to 2021 — substantially driven by new solutions like crypto-assisted remittances and digital payment options.

While instant payments are taking off faster in APAC than anywhere else, their success in the region is not guaranteed. Key contributing factors will include further blockchain and global banking platform adoption as well as close collaborations between business and government.

Let’s dive into how instant payments — both crypto and non-crypto versions — have evolved, discuss the barriers to successful implementation and what to expect next for this advancing region.

What Are Instant Payments and Why Should I Care?

Instant payments are digital transactions between participating banks that leverage an instant messaging/payments layer, allowing for real-time settlements that deliver exceptional end-user experiences. Many non-crypto instant payment networks require pre-funding beneficiary accounts to enable a real-time transfer.

A higher level of transparency — which is often unavailable in transfers from traditional financial institutions — can be achieved through digital payment rails. For example, some transactions are able to bundle the payment and payment data together using end-to-end communication flows and immediate confirmation notifications. This type of transaction is a convenient, secure way to exchange information between all parties involved. There are also various overlay services that help with ease of use and security for both domestic and cross-border payment system linkages, like linking mobile numbers to bank accounts as a way of identity verification.

Crypto-forward instant payments offer even further benefits, including increased speed and efficiency for both sender and receiver. With 24/7/365 availability, transfers can be processed at any time, including weekends and holidays. This dramatically speeds up the global flow of capital and gives consumers always-on access to their funds. In the case of transparency, payments service providers (PSPs) can further benefit from the use of services like RippleNet’s account lookup API, which allows both sender and receiver to exchange information via flexible API calls on many types of metadata, including validation of a beneficiary’s account details prior to sending a payment.

Certain crypto solutions, such as On-Demand Liquidity, also eliminate the need for pre-funding. This frees up working capital that ODL customers can then reallocate and use more efficiently to stoke additional growth. Real-time settlement and lower-cost payments in local currency are made possible regardless of funding source or destination, thanks to the flexibility of crypto (e.g. XRP) which acts as a bridge currency between sender and receiver.

The Evolution of Asia-Pacific Banking and Finance

Across the region, changes in consumer habits and impacts of the COVID-19 pandemic shed light on the evolution of instant payments into more mainstream usage.

The pandemic influenced major shifts in overall payment behaviors in APAC. While some shifts are part of global trends, like the decline of cash usage and an accelerated move from brick-and-mortar to e-commerce, others are region-specific, like the Republic of Palau’s push towards innovative, sustainable payment products and their underlying blockchain technologies. Consumer behavior has changed with COVID-19 and consumer expectations have grown alongside advanced payment solutions.

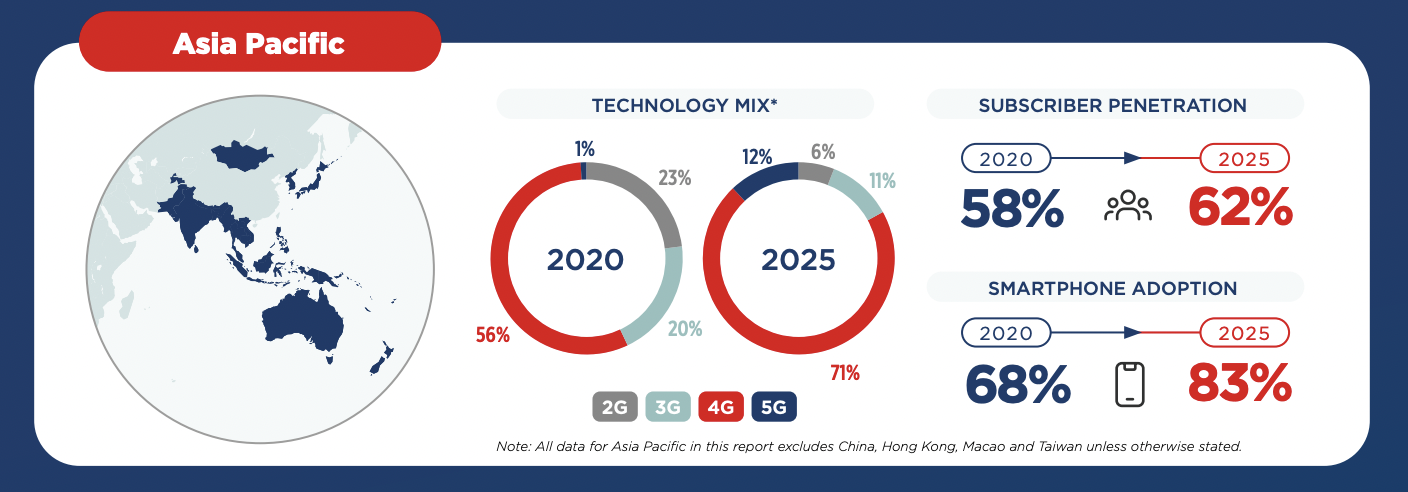

Additionally, the rise in smartphone adoption within APAC has opened up the market for the launch of new applications which enable instant payments. With smartphone usage across the region expected to reach 83% by 2025, demand for real-time payments will continue to rise across consumers and businesses alike.

(Source: Mobile Economy)

Barriers to Success

Although this region is generally progressive with new technology, privacy and security concerns remain a central barrier to the adoption of instant payment rails. Research shows that around 4 in 10 consumers across APAC are hesitant to store their financial data online and do not trust the security of these platforms, while 25% believe their personal devices lack sufficient security. In Singapore, e-commerce-related cyber crimes rose by nearly 75%, prompting the government to change data privacy laws to help combat this trend.

In years past, the region battled a lack of understanding about the blockchain technology that underpins crypto digital payments across APAC businesses. Over the last couple of years, however, we’ve seen APAC crypto adoption speed up, with an estimated 81% CAGR (Compound Annual Growth Rate) in the global blockchain market over five years at $23.3 billion USD by 2023. Among the many use cases of blockchain technology, cross-border payments comprised the largest individual use case at 15.9% globally in 2021.

That being said, the payments landscape across APAC is still highly fragmented in terms of individual country policies and regulations. There are bright spots, like the linkage of real-time payment systems in Southeast Asia between Singapore’s PayNow and Thailand’s PromptPay, but as with any industry, each country brings its own unique infrastructure and currency to work with – and the current lack of standard integration for regional cross-border payments often leads to expensive workarounds.

So What’s Next?

Appearing on the horizon of digital payments across APAC is a crossover to profitability. While only 13 of the 249 digital banks worldwide are profitable, 10 of those are based in Asia, showing that the APAC fintech sector is a proving ground for new financial services. This means that continued rapid expansion can also be expected as the region’s fintech market is anticipated to grow at 72.5% annually through 2025, showing dynamic adaptation, moving at speeds currently unmatched by Western countries.

As the use of crypto in payments continues to expand and evolve in APAC, harnessing the power of that momentum will rely on close collaboration between national governments and private companies to achieve maximum impact and drive down costs. In the wake of strong governmental support for new financial services from countries like Singapore and the Philippines, we anticipate greater guidance from regulators throughout the region. We can expect that governments across APAC will provide clarity on emerging blockchain and crypto technologies that are poised to solve payments challenges and open up new business opportunities across a fragmented yet evolving region.

The post APAC Leading the Way in Instant Payments appeared first on Ripple.